Growing older and Wise-r

The importance of Product/Brand alignment, the evolution of Wise and figuring out when to rebrand

Hey Fintechers and Fintech newbies 👋🏽

Welcome to Fintech R&R. An update to start this week’s edition. I’ve listened to the feedback submitted via the form and added ‘Favourite Tweet’ and ‘Summary of recent Fintech News’ to the end of this edition which will be a mainstay going forwards. And I’m always keen to hear your feedback, so drop it here.

Regarding the inspiration for this week’s topic, the title and the puns, Wise made that pretty easy for me, so thank you Wise team!

Specifically, their recent rebrand made me think about this tricky question, “As your product evolves, when, if at all, is the right time to rename/rebrand?”.

Pulling at that thread made me ponder brand value and alignment with product and organisation objectives.

And although the Product team isn’t directly responsible for rebranding, renaming, changing marketing materials, tone of voice etc, these things evolve based on the long-term strategic direction of the business, which works symbiotically with the growth and evolution of the product.

So as well as my favourite tweet, interesting news (and puns + movie references of course), this week includes the following:

Who and what is Wise?

Wise’s Product and Brand evolution

Other Fintech Rebrands/Renames

Reasons to Rebrand including Product evolution

Figuring out when to rebrand (if at all)

Who and what is Wise (nee TransferWise)? 🤔

Wise started life TransferWise and was launched way back in Jan 2011 by founders Taavet Hinrikus (former Chairman) and Kristo Käärmann (current CEO), with the vision of making international money transfers for individuals faster and cheaper than traditional banks.

As with many passionate founders, they were directly impacted by the problem they were trying to solve. Käärmann was working for Deloitte in London, being paid in pounds and wanted to send money back to his home country of Estonia to pay his mortgage. Taavet lived in London but was paid in Euros and needed pounds to pay bills and generally get by in London. They each needed the currency the other one had and didn’t want to be stung by long transfer times and high fees.

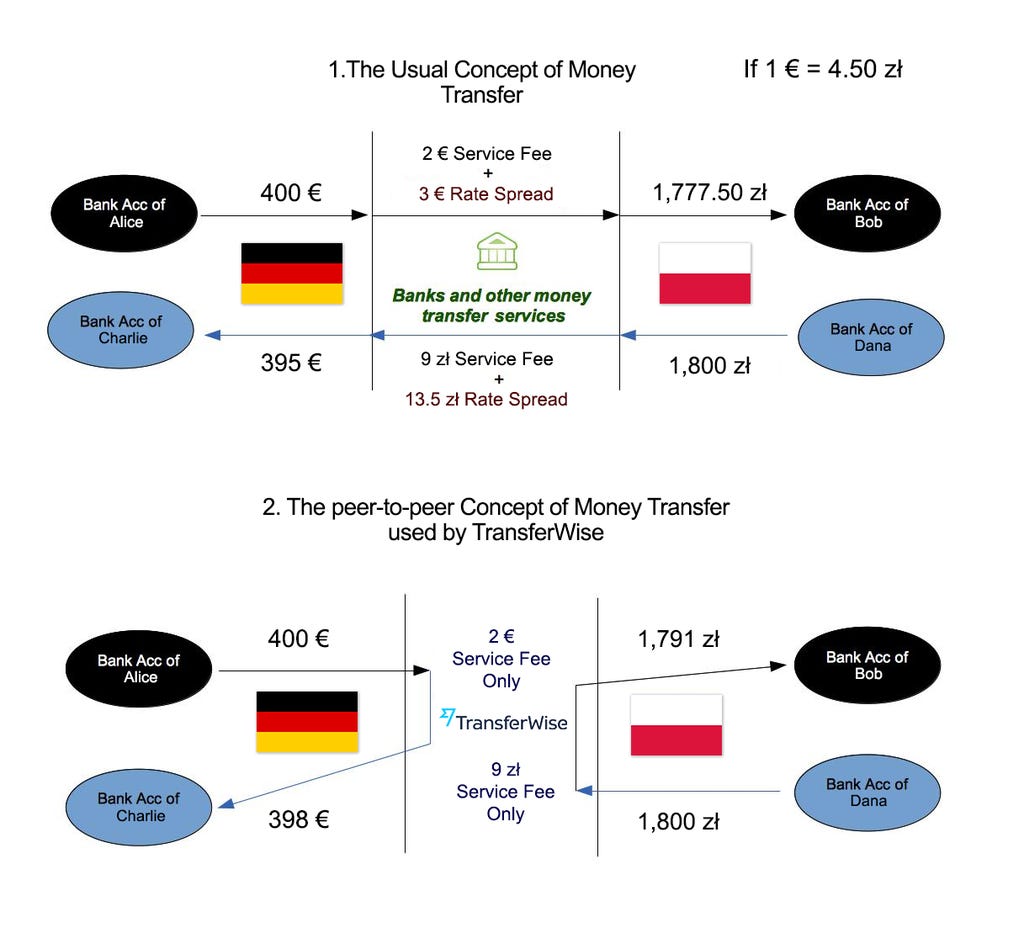

And that’s what they discussed when they met at a party in London and devised a novel way of solving the problem. Kristo would top up Taavet’s account with pounds, and Taavet would add Euros to Kristo’s account using a rate without any extra fees.

That concept of peer-to-peer transfers worked for them and is the basis of Wise’s fast and fair money transfer model.

The early, circa 2011 offering used the P2P model and supported transfers to and from GBP & EUR, charging a fixed fee for each transfer.

Over the years TransferWise grew.

Slowly increasing the number of supported currencies from the original 2 to over 50 today.

Growing its core transfer functionality by adding multi-currency personal and business accounts, debit cards, and expense tracking, amongst other features.

And growing its customer base organically and by increasing marketing efforts.

They’ve also developed Wise Platform, allowing neobanks and other fintechs to use its tech to facilitate fast and cheaper transfers rather than building this functionality from scratch.

The next steps are clear. Increase currency and country coverage, and continue to evolve and expand the Personal, Business and Platform products by increasing payment methods, reducing transfer costs, and increasing transfer speeds. And crack 2 huge markets. China and India. All of which will add to their existing 16 million customers and pursue their Big Hairy Audacious Goal (BHAG) of saving customers £180BN.

Product and Brand go hand-in-hand 🫱🏽🫲🏻

At the top, I mentioned pulling at the rebrand thread, but this edition could have covered many other areas based on the initial subject matter. A deep dive into BHAGs and their importance in uniting a company towards a single collective goal. A look into Product Vision -> Product Strategy -> Product Roadmap -> Product Backlog. Or a write-up about product-led growth. But I’m fairly sure I’ll be able to cover these topics in future editions. I couldn’t let the opportunity pass to cover a neglected area of fintech product using this shining example. It also gives me an excuse to make an image-heavy edition and include a Justin Timberlake reference…

So let’s start by looking at some of the pivotal moments in the evolution of this fintech unicorn started by two wise men over 12 years ago…

2011

TransferWise was the name they established in 2011 with their initial offering of GBP/EUR fixed fee transfers. Coming up with a startup name can be a challenge in itself because there are multiple avenues to go down, including:

A name based on the name of the founder(s). Adidas, Ford, Gillette, JP Morgan Chase and Barclays are famous examples, but this naming method is less prevalent in modern-day fintech.

A name that is slightly obscure but memorable and one which a brand and following can be built around and quickly scalable from their original product offering. E.g. Monzo, Zopa, Coconut.

A name that encapsulates principles or represents company values like trust and authority but is not necessarily directly related to the product or offering. In FS, companies like BlackRock, Fidelity and OakNorth are good examples.

A name that represents a location like HSBC, RBS, Bank of America, Bank of China.

Or a name directly associated with the service, product functionality and/or customer value. E.g. Checkout, Wagestream, PrimaryBid, ClearScore, Freetrade

Note: Check out more details about naming strategy from Frabrikbrands

It’s the latter that they went with, which relates to the product offering of simpler, smarter and fairer money transfers, therefore TransferWise.

As you can see, the logo and colour scheme reflected the early-stage nature of the startup and product at the time.

2014

By the end of 2014, TransferWise had raised over 25m in funding and gained the backing of mainstream entrepreneurs, including Richard Branson and Peter Theil (PayPal co-founder). They’d also grown to 240 employees (200 employees in 2014 alone).

In terms of product development, the progress was major.

Expansion of the number of supported currencies from the original lovestruck pair to hug family, including US Dollars, Swiss Franc, Polish Zloty, Danish, Swedish, Norwegian Krone, Chinese Yuan, Indian Rupee, Turkish Lira, and South African Rand.

The launch of an Android app in 2014 in addition to the iPhone app launched the previous year.

These product advancements, great word of mouth and campaign marketing led them to the milestone of £1 billion in cross-border payments transferred by mid-2014.

This product evolution and customer growth led them to embark on their first major rebrand, launched towards the end of 2014. This made the brand more distinctive, ensured their product could get into the hearts and minds of an even wider audience but also gave the brand a more modern look and feel and was representative of the significant progress made.

The rebrand also saw the introduction of its first on-brand symbol. The ‘fast flag’. Cementing them as the cool money transfer service.

2021

This was the most significant change in the brand and an indication of the scale of the evolution from the initial offering.

It wasn’t just a widening of the offering in terms of the number of supported currencies. But, an increase in the depth of what they were offering that significantly changed in the years since it’s the first rebrand.

And what was the change?

Yup. They dropped ‘Transfer’, becoming ‘Wise’. Or ‘Wising up’ if you will.

So why is this significant?

Because dropping the ‘Transfer’ was a public statement that they were not just a money transfer service.

By 2021, Wise had personal & business accounts to store money in multiple currencies, debit cards, multi-user access, launched in more countries and had Wise Platform, its ‘borderless-money-as-a-service’ infrastructure allowing neobanks and other fintechs to leverage its tech to serve their customers. Wise Platform allows them to scale their customer base whilst maintaining a manageable customer acquisition cost.

That’s why it’s significant. Because the product evolution clearly indicated they were moving beyond just sending and receiving money.

2023

It’s been two years since the name change. So why change the brand again?

A branding refresh was always on the cards, and I think this was part 2 of the 2-stage plan that started with the name change. The second part being aligning the brand with company and product objectives and the growing and diverse customer base.

It’s clear from the latest green refresh that global domination is the next step. From 2021 they’re not just money transfers but looking to be the go-to app for everything borderless money. Expanding the breadth of the offering to serve more countries, currencies and customers as well as the depth of the product by adding things like debit card rewards, even faster transfer times across countries, cashback for business customers and much more.

Creating a brand that aligns with a global vision and lofty products ambitions is certainly a wise move and allows them to target new segments and launch to new countries much more seamlessly.

I think the world's first globally accessible digital bank could be on the horizon…

Some other examples of Fintech Rebrands? 💳

Wise are not the only fintech to get a bit of a face lift. Here are some other examples of fintech brand/name changes over the years.

Monzo tweaked logo and early name change - Monzos birth name was Mondo. Since the change they’ve made more brand and design changes adding more human imagery, refreshed illustrations and generally making it a bit friendly to a wider audience

MarketInvoice first renaming to MarketFinance and then rebranding and renaming as Kriya - A full name and rebrand to move from pure invoice finance into more an embedded finance offering

Rapyd rebranding - Changing to a more colourful edgy brand to stand out from the other fintech players in the market

Tweaking Nubanks logo and colour scheme - Softer edges on its fonts and logo and a slightly different shade to it’s popular purple and it’s evolution reflects the bank becoming more mature and accessible to an even wider Brazilian audience

Reasons for rebranding 🎨

My intention wasn’t to turn this into a deep dive into Wise and all the reasons I think they’re great. Although I’ve clearly done a bit of that.

The point is to highlight brand evolution, the importance of timing, and the reasons behind a branding change. And even though an evolving product is one of the supremely important reasons, it’s not the only one.

Product Evolution

An obvious one and a contributing factor in Wise’s rebrand.

As a product changes from early stage MVP, finds Product/Customer & Product/Market fit and eventually expands in terms of the offering, the initial brand inevitably needs to be tweaked to fit what the new product looks like. And if the product snowballs and outgrows the initial brand, these tweaks turn into a full-blown refresh.

Pivot in Business Objectives

Businesses change objectives all the time. Whether switching from a B2C to a B2B model, doubling down on a specific part of the product and discarding others, or completely changing what the product is. This is what Instagram did when they pivoted from Burbn, a foursquare style check-in app, to the ‘instant camera’/’ telegram’ app we know and love/loathe today.

Changing Design Trends

Digital design, like fashion, has trends that fall in and out of favour. Trends usually change over time and some are a flash in the pan. For example, the use of illustrations in websites and brands has become pretty popular, but should this trend fall out of favour, it could require a branding refresh.

Much like Justin Timberlake when he went solo after N-Sync, he had to drop out of waining popstar trend and into the more popular RnB route. And to do this he needed a haircut and a change of wardrobe.

(Yes, two JT references in one newsletter)

Changing Customer Segment

Another one I’m confident contributed to Wise’s refresh.

Customer segments factor heavily in designers’ and brand agencies’ processes when creating a brand book, logo, tone of voice etc. Because building a product and brand aimed at Gen-Z differs from one aimed at baby boomers.

And as a product grows, the target customer segment becomes broader so the brand that worked when the customer profile was very specific often doesn’t resonate with the new wider base.

Is it time to rebrand/change brand? ⏰

This is the ultimate question facing a lot of fintechs and can be a dilemma. After all, changing the name and brand can be a time-consuming and costly exercise and only sometimes land the way you expected. So is there a ‘right’ time to rebrand?

As I’ve mentioned before, I’m no designer. But I have worked with many great design and brand folks and learnt a lot by osmosis. And through this learning by osmosis, I’ve come up with a list of key questions to ask and assess if thinking about a rebrand…

Is your product offering significantly different to what it was a 6 months ago and/or will it be significantly different in 6 months time?

Is there a clear roadmap showing an evolution in the product and change in direction for the next 6-12 months?

Does your brand look dated or stale compared to competitors?

Was the last time the look and feel was updated greater than 5 years?

Have you had significant customer growth over the past 3 years?

Have you expanded to new geographies and different cultures since your last brand update?

Has the business changed its model?

Is the organisation focussing on B2B rather than B2C or vice versa?

Have your regional customer segments considerably changed over the last year?

Are you looking to target or launch to a region or segment with significant cultural or social differences to the existing customer base?

Are your design and brand still based on what was used during MVP?

If the answer to the majority and, god forbid, all of them is yes, then the odds are you need to at least think about updating your design and brand.

Obviously this is not a simple task and doesn’t just involve the product team.

It’ll require a deep dive into the medium and long term product roadmap, a review of the company objectives (looking historically and into the future), a look at the competitive landscape and probably engaging external voices like brand agencies and consultants.

But if you get it right, continue to refresh your brand and maintain one that aligns with your organisation, product, customer base and ambition you’re making wise moves for future growth and scale. 💪🏽

Interesting Fintech News w/ My Comments

Klarna loses 1 Billion - Pretty big wad of cash to lose. But they’ve said they’ll return to profitability in 2023. Although they didn’t explain how…

Griffin gets a banking licence - The banking-as-a-service technology provider was recently granted a banking licence from the FCA meaning they can customer deposits. It’s the UK’s first ‘BaaS Bank’ and I think it’ll make them a big draw when it comes to selecting a banking service provider

Candidly gets $10.5m in funding - The US student debt and savings optimisation looks to capitalise on it’s recent growth. This recent surge in US based student finance platforms (Frank covered last week) could accelerate the disruption of the student finance monopoly here in the UK. We can only hope

Favourite Tweet

This tweet encapsulates why customer journey mapping is essential. Especially if you’re the PM and want to seem like you’re ‘doing innovation’