BVNK: Bvnking on Stablecoin

A deep dive tracing BVNK’s journey from 2021 to today, unpacking its product stack, exploring the value of infrastructure, and mapping how stablecoins will go mainstream.

Hey Fintechers and Fintech newbies 👋🏽

In the last edition, I wrote a detailed stablecoin primer.

It covered the history of money, the eras that led to key upgrades, from barter, commodities, and metal coins, to paper, cards, and finally, crypto, highlighting that each era solved shortcomings of the one before it and alluded to stablecoin as the next key solve for the internet era.

I also broke down what a stablecoin actually is (and how it differs from Bitcoin), explained the “Cryptocurrency Layer Cake” from Layer 0 to Layer 3, compared stablecoin enablers to their TradFi counterparts, and highlighted use cases beyond remittances, like cross-border B2B payments and payroll for the global gig economy.

During the deep dive, I highlighted organisations enabling innovation in the different layers, and one that stood out because of their coverage across the stablecoin stack, and the partnership news that came out as I was writing was…BVNK.

BVNK is a full-stack stablecoin solution founded in 2021, with infrastructure built from the ground up that processes $18B $19B ~$20B in annualised payment volume for clients like Worldpay, Deel and dLocal, and they’ve just had their 4th birthday. 🎉

NB. A neat demonstration of their growth is the fact that I had to update the annualised payment volume number three times in three weeks with the $20B figure crossed days ago, hence the strikethroughs.

Following on from the stablecoin primer and with the onslaught of stablecoin news, including the recent news about Tempo, it felt like the perfect time to do a classic fintech deep dive into a company with a full-stack solution enabling native and bridging stablecoin innovation, and doing it for nearly 5 years (which in Stablecoin years feels like a lifetime).

Here’s what to expect:

BVNK Background

A timeline of key events from 2021-Present Day

Interesting recent product launches

BVNK’s Product Stack

Send

Receive

Store

Convert

Spend (In progress)

Earn (In progress)

Nuance of Layer1 (Self-Managed) and a managed service

The Currency of Infrastructure

Now, Next, Later: The Stablecoin Adoption Roadmap

The Stable Rail Switchpoint

Now let's get into it 💪🏽

💡 This newsletter has been kindly sponsored by BVNK, who provided some up-to-date numbers and product releases but has been written independently and with creative freedom (as you’ll be able to see throughout).

For readers unfamiliar with my musings, I tend to include movie references and weave in a few puns so keep your eyes peeled for THE perfect Wallace and Gromit x Stablecoin referenceP.S. You know the deal by now. This is a very deep, deep dive, so click here to read the full version as your email client may clip the end, which you do not want to miss.

Bvckground

BVNK (pronounced B.V.N.K) is a full-stack stablecoin infrastructure provider building the infrastructure layer for businesses that want to integrate stablecoin payments into their operations and build stablecoin products for the internet era.

Founded in 2021, BVNK set out with a clear goal.

To make stablecoins usable at scale for financial institutions, fintechs, enterprise platforms and corporates.

While crypto exchanges and DeFi protocols had already embraced stablecoins, there was no full-stack provider making them enterprise-ready with licensing, compliance, orchestration, and integration tools all in one platform.

BVNK spotted that gap.

The company rightly positions itself as a crucial connector between TradFi and digital assets.

On the one hand, it offers the licensing, fraud controls, and compliance frameworks that large enterprises expect. On the other hand, it delivers crypto-native infrastructure including stablecoin wallets, on/off-ramps, orchestration APIs, and settlement rails that operate 24/7, across borders, and at a fraction of the cost of ‘traditional’ networks.

The inception of BVNK has echoes of fintech unicorns of the past.

Highly experienced, driven individuals, operating in an area for a while, who directly feel the pain at the sharp end of the problem, eventually band together to solve it themselves.

In this case, the problem was how poorly suited traditional financial rails are for modern, digital-first businesses. Even as companies globalised and consumers shifted to mobile-first platforms, payments were still constrained by slow settlement times, high fees, and heavy reliance on correspondent banking. For founders operating at the intersection of fintech and crypto, the shortcomings were especially stark:

Cross-border flows were costly, opaque, and too slow to support digital-native commerce.

On/off-ramps between fiat and stablecoins were fragmented, requiring multiple providers and manual integrations.

Compliance and licensing were complex and inconsistent across jurisdictions, making it hard to scale globally.

Infrastructure gaps meant every company had to rebuild the same wallet, custody, and orchestration systems from scratch.

BVNK’s founding team had lived this pain directly, working in fintech, banking, and digital assets, and recognised that the lack of enterprise-grade infrastructure for internet native money was holding back adoption. By bundling licensing, payments, wallets, and orchestration into one stack, they set out to create a ‘one-stop shop’ for stablecoin. A single platform where businesses can build, launch, and scale stablecoin-powered products without reinventing the wheel.

Jesse Hemson-Struthers (Co-Founder & CEO) -> Serial fintech entrepreneur who had already built crypto exchanges and payments platforms, giving him firsthand experience with the pain of integrating stablecoins into regulated, enterprise-grade payments. Former CEO/Founder of Coindirect.

Chris Harmse (Co-Founder & Chief Business Officer) -> Trained as a chartered financial analyst and became a respected authority in the stablecoin infrastructure space and digital asset innovation, Chris co-founded BVNK to help enterprises accelerate global money movement through blockchain technology. Chris’s experience on the trading desk at BNP Paribas (similarly to my experience at Citibank) where he saw huge volumes of trades being executed in milliseconds but the challenges that are brought with varying settlement times depending on the type of trade and the extra admin of reconciliation for back office.

Donald Jackson (Co-Founder & CTO) -> A veteran technologist in blockchain & enterprise systems, who led the build of BVNK’s Layer1 infrastructure & Smart Treasury, turning what was once complex, backend-heavy stablecoin plumbing into modular, scalable tools businesses can plug into. He’s also leading the build of machine learning capabilities into stablecoin infrastructure. Previously founded “Cue” (a customer engagement platform) and “Verity,” a fraud-reduction service.

Adding to the founding team's deep expertise, BVNK brought in leaders with equally strong pedigrees across finance, payments, and compliance. Phil Doyle (Chief Compliance Officer) brought nearly two decades of fraud and compliance experience, having held senior roles at Revolut, Visa, ClearBank, and Zepz. Darran Pienaar (CFO) brought heavyweight financial oversight, having led finance teams at Ebury as well as large, publicly listed companies like Marks & Spencer and Tesco. And Emma Mayer (CMO) brought in over a decade of marketing experience, with her most recent leadership experience gained at open banking infrastructure provider TrueLayer as their VP of Marketing.

Just like the Plaid founders in 2013, the Marqeta founder in 2010 and many others, they used their previous experience in financial services innovation, with Jesse and Chris’ Coindirect experience proving valuable, and decided to zoom out to look at the bigger problem.

Building the missing infrastructure that enables traditional companies to innovate with and embed digital currency into their stack.

The Plaid founders built infrastructure that enabled innovation and transformation using banking data that led to transformed lending journeys, personal finance management and pay-by-bank volumes.

Marqeta built infrastructure that enabled fintech card and payment processing innovation leading to new digital challenger banks, expense management products and embedded card programmes.

And BVNK set out to build the infrastructure that would do the same for stablecoins. While Plaid unlocked innovation through data and Marqeta through cards, BVNK’s mission was to make stablecoins enterprise-ready, giving traditional businesses the rails, safeguards, and APIs to embed digital currency directly into their products and operations.

Just as previous generations of infrastructure companies paved the way for entirely new categories of financial products, BVNK’s founders saw stablecoins as the next logical upgrade to money, but recognised that adoption would stall without an enterprise-grade connector between TradFi and crypto and there was no full-stack, enterprise-ready stablecoin partner that could offer the regulatory safeguards of TradFi while unlocking the programmability, speed, and borderless settlement of digital assets.

That was the gap BVNK set out to fill.

💡Fun fact: Their ambition of filling that gap in the future of money is directly reflected in their name which is a fun play on the word bank with the ‘A’ flipped upside down reflecting their infrastructure for the new age of internet native money.

A timeline of BVNK from A to V 🔠

From identifying a gap in enterprise-ready stablecoin infrastructure to powering payouts, pay-ins, and conversions for global fintechs and corporates, BVNK has grown rapidly in just a few years. Their journey mirrors other infrastructure pioneers but this time the mission is to make stablecoins usable at scale, and from their initial founding in 2021 they have expanded their product, client base, transaction volume and .

2021: Founding & Early Vision

Launch: BVNK is a global business with the goal of bridging the gap between stablecoin adoption in crypto-native markets and the needs of financial institutions, fintechs, and enterprises.

Problem Identified: Stablecoins were thriving in DeFi and exchanges, but there was no enterprise-ready infrastructure offering licensing, compliance, and orchestration tools. BVNK set out to fill that gap.

Seed Funding: Raised ~$12M seed round led by Kingsway Capital (with participation from Tiger Global), validating the thesis of building a full-stack stablecoin enablement platform.

2022: Product Foundation & First Clients

Core Stack Launched: BVNK introduced its managed payments platform, offering APIs for stablecoin Send, Receive, Store, and Convert, a full-stack approach unusual for the market at the time.

Compliance First: Secured regulatory approvals and licences in the UK and EU, positioning itself as a trusted counterparty for regulated institutions.

Early Clients: Attracted fintechs and digital banks exploring stablecoin rails for cross-border payments and treasury diversification.

Series A: Raised $40M led by Tiger Global, showing strong investor confidence in scaling stablecoin infrastructure.

2023: Expansion & Industry Recognition

US Market Entry: Began the process of entering the US market, setting up state-by-state licensing frameworks and striking early partnerships.

Enterprise Adoption: Signed up digital-first banks, fintechs, and B2B platforms using stablecoins for payouts and FX conversion.

Strengthened Infrastructure: Expanded partnerships with custodians, liquidity providers, and networks to ensure stable settlement rails.

Industry Profile: Recognition as one of the emerging “full-stack stablecoin operators,” mentioned alongside Circle and Fireblocks in ecosystem maps.

2024: Scaling & Deepening the Stack

Geographic Reach: Expanded global footprint with coverage across Europe, Africa, Asia, and LatAm.

Product Evolution: Enhanced Convert to support real-time FX across stablecoins and fiat, improving B2B payment and treasury use cases.

Team Growth: Hired senior leaders from Revolut, Visa, PayPal and Currencycloud, strengthening expertise across compliance, payments, and financial operations.

Enterprise Wins: Attracted large-scale enterprise clients exploring stablecoin treasury and embedded account solutions, including but not limited to Deel and Rapyd.

Layer1 Launch: Introduced Layer1, a self-hosted, enterprise-grade stablecoin infrastructure giving clients direct control over wallets, custody, and integration while removing reliance on third parties, and making it simpler for businesses to own and manage their stablecoin offerings.

2025: US Nationwide Rollout & Full-Stack Ambition

50-State Coverage: Announced availability across all 50 US states, including New York, via a mix of its own licences and a Paxos partnership.

High-Profile Clients: Signed deals with Xapo Bank, Flywire, Worldpay, dLocal, Ferrari and Bitso, demonstrating traction across both fiat-first enterprises and crypto-native players.Product Roadmap: Revealed upcoming Spend (stablecoin-linked cards) and Earn (yield on stablecoin balances), expanding into everyday payments and treasury optimisation and also added embedded wallets into their offering, deepening the ‘Store’ part of their product stack.

Positioning: Now positioned as the enterprise-grade stablecoin operating system. A full-stack solution for businesses to embed stablecoin into payments, treasury, and financial products.

At time of writing, they’ve processed ~$20B in transactions, powering flows for a diverse set of clients from global banks experimenting with digital treasury, to fintech disruptors embedding stablecoin wallets into their platforms, to cross-border trade and remittance platforms chasing faster settlement, and crypto-native firms bridging liquidity across chains and markets.

And in just four years (they blew out 4 candles on their very recent birthday), BVNK has gone from identifying a glaring infrastructure gap to powering the tools that make stablecoins usable in enterprise payments, treasury, and financial services.

There’s a lot to dissect from the packed timeline but there are a couple of key releases from their recent history that stand out to me.

Key ‘Recent’ Product Launches 🚀

Layer1 - Enterprise-Grade Infrastructure

What it is: A self-custody infrastructure product that allows enterprises to run their own stablecoin stack including wallets, keys, integrations, and reconciliation, under their direct control.

In simple terms, it’s like giving a bank or fintech its own “crypto data centre”, complete with all the tools to issue wallets, move, and manage stablecoins, without relying on third parties.

🤔 Why it matters: One of the biggest blockers for enterprise adoption of stablecoins has been reliance on third-party custody and fragmented providers. With Layer1, BVNK shifts the paradigm so businesses can own and control their infrastructure rather than plug into it which is critical for regulated institutions that need security, compliance, and independence baked into their digital asset operations. It’s also built natively for high-velocity payments, rather than adding payments infra as an afterthought.

Earn - Stablecoin Yield

What it is: Yield products that enable businesses to earn returns on stablecoin balances, powered by short-term treasuries or other low-risk instruments.

In simple terms, it’s like putting your stablecoins into a high-yield savings account that generates income rather than losing value to inflation much like a savings account for businesses that earn interest on cash balances.

🤔 Why it matters: Treasury optimisation has always been a key driver for enterprise adoption. For CFOs, idle cash is a cost. Earn transforms stablecoins from just a settlement tool into an asset that can generate safe, predictable yield while remaining highly liquid. It’s a direct answer to the question: why should I hold stablecoins on my balance sheet?

Spend - Stablecoin-Linked Cards

What it is: Stablecoin-powered cards that allow businesses (and their customers) to spend stablecoin balances seamlessly in the existing card network ecosystem.

In simple terms, it turns stablecoins in a wallet into something you can swipe, tap, or use online just like a normal card with zero difference to the consumer’s regular payment habit.

🤔 Why it matters: This bridges the gap between the “old rails” and the “new rails”, an analogy I’ll refer to again later. Enterprises can hold value in stablecoins but still transact in the fiat world through card rails without friction. For end users, it turns stablecoins from a treasury tool into something usable in everyday life.

For me, ‘Spend’ and stablecoin linked to cards is the biggest game changer and true connector of the fiat and stablecoin world for the consumer. In my opinion, it’s where the majority of FS companies taking their first steps into stablecoin will look to innovate as it means innovating in the backend rails whilst having no negative impact to the consumers current way of paying for goods and services.

Bringing these three together, Layer1, Spend, and Earn represent BVNK’s evolution from a payments enabler into a full-stack stablecoin operating system. Layer1 solves for enterprise-grade infrastructure, Spend embeds stablecoins into everyday payments, and Earn transforms them into productive treasury assets. It’s this trifecta, infrastructure, utility, and value creation, along with its already established core product suite that positions BVNK as one of the few players building the connective tissue between TradFi credibility and internet-native finance.

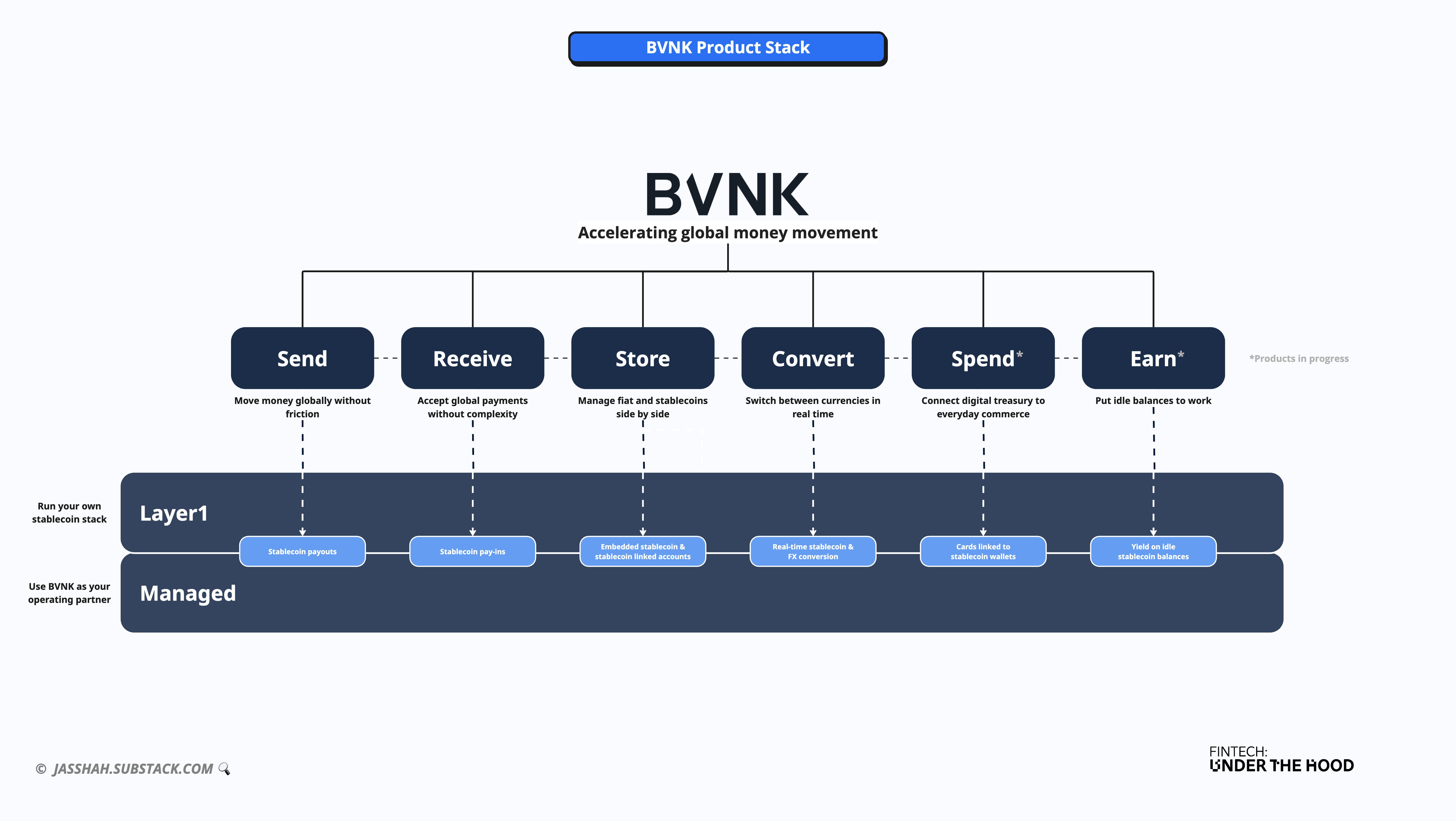

BVNK’s Product Stack 🍰

A big driver behind BVNK’s growth has been its complete yet modular platform, a design philosophy shared by many modern financial infrastructure providers. Rather than forcing clients into an all-or-nothing stack, BVNK offers the building blocks of stablecoin infrastructure in a way that’s both flexible and enterprise-ready.

Clients can pick and choose what they need. Some start with the infrastructure layer, wallets, custody, and stablecoin rails. Others lean on the payments layer, acceptance, orchestration, and merchant settlement. Each module can be fully managed by BVNK or self-managed by the client, giving businesses the option to embed stablecoin services under their own brand, striking the right balance of control and support.

The result is a suite of products that mirror how businesses already interact with money, storing, spending, earning, and moving value across systems. This modularity not only lowers barriers to entry but also scales with client needs, from initial experiments to full-stack adoption. Here are the six core components of their stack.

1. Send - Move money globally without friction

👉🏽 Stablecoin payouts make global payments instant, low-cost, and transparent. Whether paying suppliers, contractors, or employees, BVNK turns a process that normally takes days into seconds.

Stablecoin payouts - Send funds directly in stablecoins across borders, bypassing the delays and costs of correspondent banks.

🧠 Example: A global freelancer platform pays thousands of workers in stablecoins, giving them same-day access to funds instead of waiting for international wires.

2. Receive - Accept global payments without complexity

👉🏽 Accepting funds in stablecoins is critical for merchants and fintechs serving global customers. BVNK provides a compliant, enterprise-ready way to do this without the complexity of managing wallets or custody.

Stablecoin pay-ins – Accept payments directly from customers in stablecoins like USDC or in traditional fiat currencies, with funds automatically reconciled.

🧠 Example: An online marketplace accepts stablecoin payments from international buyers and converts them instantly into fiat for sellers.

3. Store - Manage fiat and stablecoins side by side

👉🏽 BVNK gives businesses secure wallets to hold balances in stablecoins or linked fiat. This acts like a digital treasury, enabling enterprises to manage their working capital in one place.

Embedded stablecoin accounts – Provide customers or internal teams with stablecoin wallets, tracked and managed like traditional bank accounts.

Stablecoin-linked fiat accounts – Offer dual fiat and stablecoin wallets that allow balances to be held, converted, and reconciled seamlessly.

🧠 Example: A digital bank embeds BVNK-powered wallets to let customers manage fiat and stablecoins side by side within their mobile app.

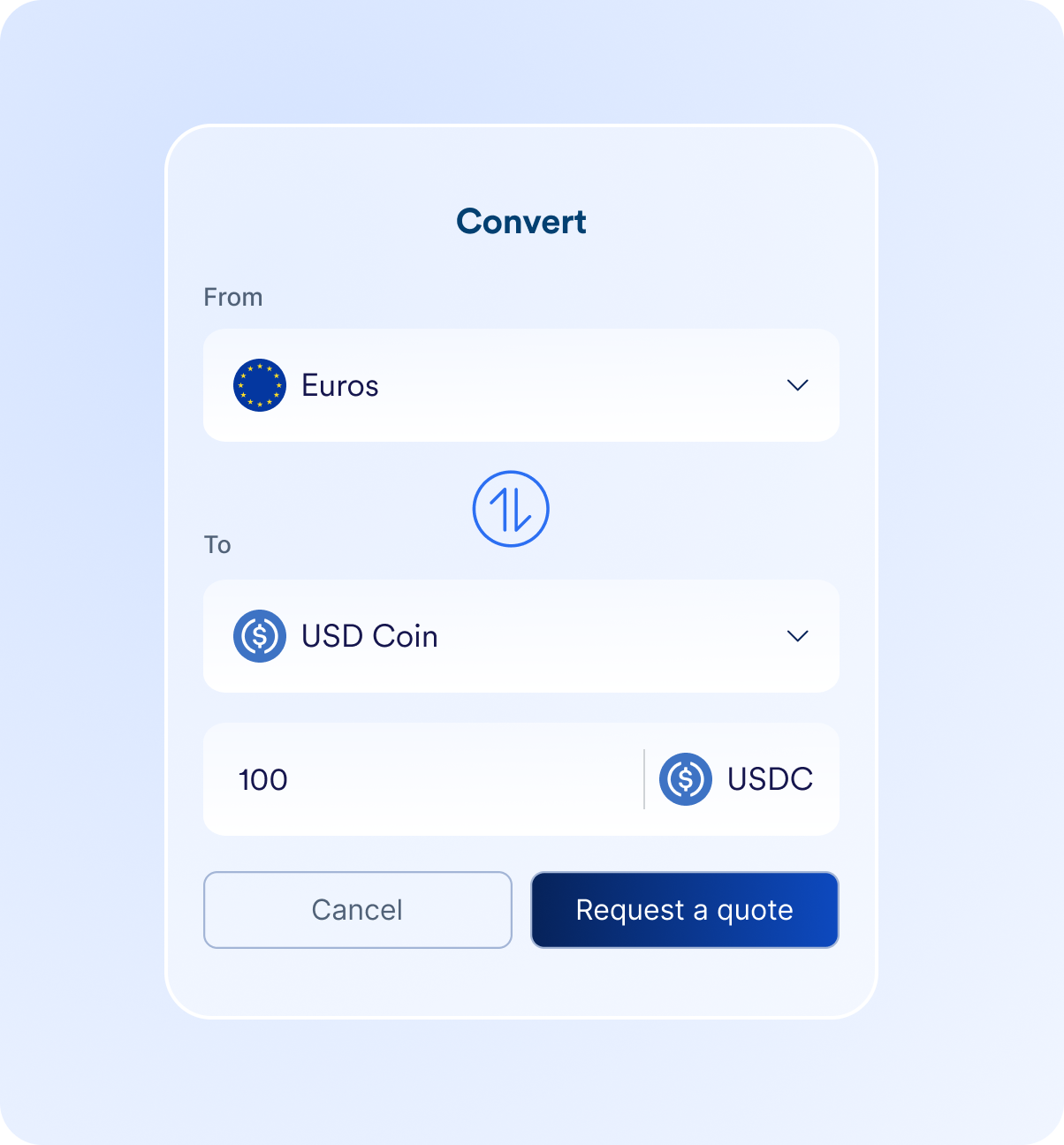

4. Convert - Switch between currencies in real time

👉🏽 Global businesses can’t afford to be trapped in a single currency. BVNK’s real-time conversion ensures stablecoin and FX flows are seamless, giving enterprises flexibility and predictability.

Real-time stablecoin & FX conversion - Instantly convert between stablecoins and fiat currencies at competitive rates and swap between different stablecoins (e.g. USDC ↔ USDT ↔ USD/EUR/GBP) to optimise liquidity and reduce counterparty exposure.

🧠 Example: A multinational business receives USDC from clients in Asia and converts it instantly into euros for European payroll.

5. Spend (In progress) - Connect digital treasury to everyday commerce

👉🏽 BVNK is building the rails to connect stablecoin balances directly to everyday commerce. By linking cards to stablecoin accounts, businesses and their teams can spend seamlessly from their digital treasury.

Cards linked to stablecoin wallets – Enable employees or customers to spend directly from stablecoin balances, anywhere traditional cards are accepted.

🧠 Example: An Employer of Record issues stablecoin-linked cards to its contractors, allowing them in different countries to spend from their USDC payouts without waiting for payroll wires.

6. Earn (In progress) - Put idle balances to work

👉🏽 Idle balances don’t have to stay idle. BVNK plans to offer yield on stablecoin holdings, helping businesses generate returns while maintaining liquidity.

Yield on idle stablecoin balances – Deploy stablecoin reserves into safe, liquid assets (e.g. short-term treasuries) to generate predictable income.

🧠 Example: A fintech platform offering embedded accounts allows customers to automatically earn yield on their stablecoin holdings, turning deposits into a revenue-generating feature.

All these modular services can be utilised in two different ways, depending on the client's wants and needs.

Self-managed (Layer1) payments – Run your own stablecoin stack

👉🏽 For enterprises that need full control, Layer1 provides self-custody infrastructure. It lets businesses manage wallets, private keys, and integrations in-house, while still leveraging BVNK’s APIs for orchestration and settlement.

Self-custody infrastructure - Enterprises run their own stablecoin rails with full regulatory oversight.

Custom integrations - Plug stablecoins directly into internal treasury or payments systems.

🧠 Example: A multinational bank deploys Layer1 to run stablecoin rails internally, enabling instant client transfers while keeping custody and compliance in-house.

Managed payments - Use BVNK as your operating partner

👉🏽 Not every business wants to run its own infrastructure. With BVNK Managed payments, clients get the benefits of the full product stack, compliance, custody, fraud controls, orchestration, delivered as a service.

Full-stack managed service - BVNK runs the infrastructure, while businesses launch stablecoin-enabled products under their own brand.

Licensing & compliance - BVNK covers regulated requirements so clients can go to market faster.

🧠 Example: A payments company embeds stablecoin payouts into its platform using BVNK’s managed stack, launching in weeks instead of months.

Each of these modules represents a fundamental infrastructure upgrade to how money moves in the internet era.

👉🏽 With Send and Receive, businesses replace clunky SWIFT messages and multi-day settlement with instant, programmable money flows.

👉🏽 With Store, treasuries evolve into multi-currency digital wallets that manage fiat and stablecoins side by side.

👉🏽 With Convert, businesses unlock real-time liquidity management across currencies and chains.

👉🏽 With Spend and Earn, stablecoins become directly useful in commerce and treasury, turning balances into both utility and yield.

👉🏽 And with Layer1 or Managed, BVNK offers enterprises the choice. Run it yourself, or let BVNK run it for you.

This modularity is what has driven BVNK’s growth. offering a stack flexible enough for fintech disruptors, but robust enough for banks and enterprises.

And there’s a reason I repeat the value of modularity and core infrastructure. It’s because historically modular infrastructure has been crucial to supercharging new eras of technological innovation.

The Currency of Infrastructure 💱

The reasons I referenced an issuer-processor and an open banking infrastructure provider as comparative examples earlier are two-fold.

Firstly, they did what the BVNK team did and moved from B2C propositions to underlying B2B players.

Plaid did it when the founders built a Personal Finance Management product back in 2012, but realised the bigger industry challenge was actually getting the data, so they pivoted to building the connective infrastructure for financial data.

And the Marqeta founder decided against building a B2C card product and instead built the modular issuer-processor that allowed many fintechs, such as challenger banks, lenders, and expense management products, to build card products and process payments.

The second and more important reason for the reference was to highlight the value of timely, full-stack, modular infrastructure to innovation eras.

There are many factors that go into ushering in and enabling eras of innovation:

Consumer behaviour – Consumer-facing innovation only happens when behaviour starts to shift. For example, without the gradual adoption of internet banking in the 2000s, the leap to fully digital banks may have been too much, too soon.

Technology readiness – It’s not just consumer demand, but whether the underlying tech can scale. Smartphones, APIs, and cloud infrastructure created the rails that made digital banking possible. Without them, even willing consumers would have faced clunky, broken experiences.

Capital availability – Waves of innovation also coincide with capital cycles. Investor appetite funds the experimentation phase and accelerates winners. Think of the neobank explosion of the 2010s, fuelled by venture funding.

Regulation – Regulation is seen as one of the big ones, and rightly so. It sets the boundaries for what can be built and creates a fertile environment for innovation to thrive.

Although regulation is one of the biggest factors in fostering a positive environment for innovation, history shows that regulation alone does not guarantee innovation. Regulation + modular technological infrastructure that meets regulatory standards is what really enables an ecosystem to flourish.

For example, even with consumers getting familiar with internet banking, and the regulation around e-money accounts going mainstream after the 2008 financial crash, the digital banking era wouldn’t have been possible with core banking infrastructure providers like ThoughtMachine and issuer-procesers like Marqeta that lowered the friction to innovate and sped up the time to market for many.

Similarly, despite the Open Banking Regulation beginning in 2009 and formally introduced in 2018 in Europe, many Personal Finance Management apps, optimised lending journeys, and Open Banking-powered B2B payments companies wouldn’t exist without the likes of Plaid, TrueLayer, Tink and others providing the vital connective infrastructure.

Stablecoins are at a similar juncture today.

Regulation is starting to take shape with the GENIUS Act in the US and equivalent discussions in Europe and Asia, consumer awareness is rising beyond crypto-native circles, and enterprises are showing real appetite to experiment with stablecoin-based payments and treasury.

But the missing link, as was the case in those previous eras, is modular tech infrastructure that allows anyone to innovate without having to build all the underlying functions themselves.

That’s why I think the big winners of the stablecoin era will be those, like BVNK, that abstract away the complexity and make stablecoins enterprise-ready, compliant, and modular enough to build on.

Hence why infrastructure itself is a valuable currency in the stablecoin era.

Now, Next, Later: The Stablecoin Adoption Roadmap 🛣

We’ve gone through the inception of BVNK, a timeline of key events, all the way to its 4th birthday, and provided a deeper look at its product stack, highlighting its importance.

Now to the subject to close this deep dive, and it is, of course, an important one.

Adoption.

If there’s one lesson I’ve learned over the past ~20 years of building products across financial services, it’s that cracking adoption is half the battle. Technology, infrastructure, and regulation are essential, but without adoption, they remain potential, not reality.

And right now, with the growing trend of using cards as the consistent end payment mechanism while “stable-ising” the backend rails, we’re seeing the adoption challenge being solved in real time.

It’s a clever transitional mechanism.

Keep what’s familiar at the front-end, while rewiring the money movement behind the scenes.

Cards are just the first act of what I think is a three-stage gradual adoption of stablecoin, so it’s the perfect way to close out using a classic Now, Next, Later roadmap format.

Now: What's driving adoption today

Next: What will drive adoption in the near term (12-24 months)?

Later: What will be the main driver of adoption in the future?

Now: Cards as the key transition mechanism 💳

Cards are the key that unlocks today’s adoption puzzle (pun fully intended). They provide a familiar wrapper for something unfamiliar: stablecoins. For consumers, tapping a card, entering details online, or swiping at a terminal doesn’t feel like a new behaviour. For businesses, linking cards to stablecoin balances means they can enable spending from a digital treasury without retraining users or waiting for global wallet adoption.

This is why the biggest players are leaning heavily into card-linked stablecoin solutions. Visa and Mastercard are piloting stablecoin settlement. PayPal and Stripe are embedding stablecoin acceptance. And BVNK is working on stablecoin-linked cards for global businesses. Cards provide a consistent user experience, mask backend complexity, and buy time for infrastructure to mature.

🧠 Imagine…going to a store and paying with a stablecoin or crypto card that immediately converts select currency into FIAT so you can tap with a card in person or use that card online (you don’t have to imagine too hard, as that’s live with numerous crypto exchanges).

👉🏽 Cards are the Trojan horse that gets stablecoins into everyday spending.

Next: Wallet Payments 📱

The next 12–24 months will see wallets take centre stage. If cards are the on-ramp, wallets are the first true stablecoin-native experience. Already, consumer wallets like MetaMask and Coinbase Wallet have tens of millions of users, and fintech platforms are embedding stablecoin wallets directly into their apps.

For merchants, wallets mean instant settlement and reduced costs. No interchange, no multi-day settlement cycles. For users, wallets offer a payment experience that’s as seamless as Venmo, Alipay, or Apple Pay — except they work across borders and around the clock. Imagine clicking “Pay with USDC” at checkout on Shopify or sending money directly to a supplier’s wallet address in seconds.

Wallets are also programmable. That means invoices can pay themselves, subscriptions can settle automatically, and treasury operations can rebalance in real time. Once users get comfortable with wallets, stablecoins will no longer need the disguise of cards.

🧠 Imagine…you’re browsing on your phone, you see tickets for a Coldplay concert in Berlin, and pay with your MetaMask wallet (with two taps and a verification) and aren’t penalised with any cross-border exchange rate fee.

👉🏽 Wallets make stablecoins feel like money reimagined for the internet, not just a backend upgrade.

Later: AI & Stablecoin 🤖

Looking further ahead, the real step-change in adoption will come from AI. As agentic systems move from novelty to everyday tools, they’ll need to transact autonomously, paying suppliers, managing subscriptions, sending remittances, or optimising treasury flows. Stablecoins, with their speed, programmability, and global reach, are the obvious solution.

And we’re already seeing the early shoots of this future.

The recent announcement with BVNK joining Mesh, MetaMask, Coinbase and others to collaborate on Google's new open standard for AI payments is testament to that.

Google’s Agentic Payments Protocol (AP2) enables AI assistants to securely handle transactions. It delivers:

Clear accountability for AI payments

Support for traditional networks and blockchain

Verifiable credentials and mandates

Secure pathways for everyday commerce

It’s not just for stablecoins as it’ll support different payment types from credit and debit cards to real-time bank transfers, but stablecoins are the obvious step with their programmability and digitally native features, and Donald, BVNK CTO agrees.

“Stablecoins provide an obvious solution to the scaling challenges agentic systems are already facing with legacy financial infrastructure. We at BVNK were extremely excited to hear that Google has been working on solving this problem and couldn't wait to contribute.” - Donald J., CTO at BVNK

As AI begins to manage more of our financial lives, from payroll to procurement, stablecoins will be the rails that make it possible. Cards won’t cut it, and wallets alone won’t scale. Stablecoins, embedded natively into AI protocols, will.

🧠 Imagine…using an AI chat layer to create a dedicated agent that scours the global ecommerce market for a special Labubu, gives limited access to a wallet with a ringfenced stablecoin amount of what your willing to spend (e.g. 50USDC), and lets the temporary agent continuously scan and execute the purchase on your behalf without you spending hours/days searching.

👉🏽 AI will make stablecoins not just mainstream, but inevitable.

That’s the roadmap:

1️⃣ Cards build trust

2️⃣ Wallets bring efficiency

3️⃣ And AI makes stablecoins default.

Switching Rails: Preparing for the Inevitable Switchpoint 🚉

What’s fascinating about this moment in payments history is that two types of organisations seem to be emerging:

The Cautious Builders – These are the incumbents quietly preparing rails in case stablecoins take off. They’re not shouting about it, but they’re laying down the groundwork so they can flip the switch if consumer demand shifts. To them, stablecoin infrastructure is like an insurance policy rather than a strategic bet.

The True Believers – Then you have the firms actively betting on stablecoins as the internet-native currency of the future. BVNK, Circle, Stripe, and PayPal aren’t building “just in case.” They’re embedding stablecoins into their core strategy and enabling others to do the same. For these players, stablecoin isn’t a hedge, it’s the rails. They see it as inevitable that money will move like data — instantly, globally, and with programmability baked in.

At some point, there will be a switching moment, the digital equivalent of changing tracks mid-journey.

It’s something that happens more often than you think with technology platforms, where underlying digital transformation is built in parallel, the rails are switched, and if it’s done well, consumers are oblivious (when a digital bank switches a payment processor, for example).

For years, the front-end (cards, bank accounts, fiat balances) will look the same, masking the rewiring underneath. But once enough infrastructure is in place, enough wallets are live, and enough AI systems rely on stablecoins for real-time commerce, the switch flips.

Stablecoin rails will no longer be the parallel track. They’ll become the main line.

NOTE: I couldn’t resist a track switching reference from one of my favourite childhood movies, and it’s the perfect visual for the future switching moment.

That’s why BVNK’s role matters.

By abstracting away the complexity and building enterprise-grade modular infrastructure, they’re enabling the Cautious Builders to experiment so they don’t get left behind, and allowing the True Believers to innovate at pace and scale.

Broadly, they’re making it possible for entire industries to be ready when the switch happens.

Because laying down new tracks while the train is already moving is tough, and as has been proven time and time again throughout the history of innovation eras, it's infrastructure players who understand the complexity and make it easy to build the tracks that are true accelerators of those eras

And BVNK has built just that for stablecoins.

That's it from me. I hope you enjoyed this deep dive 👋🏽

Remember to hit the thumbs up below, drop a comment and share it with a friend or colleague, and if you haven’t read my stablecoin primer yet, go check that out next!

Jas

P.S. If you want to partner with me on a Fintech Product deep dive or are interested in working with me in any of the below areas, reply to this or send an email to jas@bitsul.co.uk 😊 :

👉🏽 Fintech Product Strategy/Development consulting

👉🏽 General Fintech advisory

👉🏽 Digital bank building and growth advice

👉🏽 VC/Family Office product due diligence

👉🏽 Mentorship or a ‘product therapist™️’ for your team

Forget All About Stable Coins 🪙; Get The US Dollar Back Upon A Good Footing.

Great one JAS.

A look into the future. I’ve been paying in SEA through my card using “stables” and it works seamlessly

The Future is now and we are seeing how its Built. This is exciting!