Fintech R&R☕️👻 - The Paradox of Choice and the benefits of Scare-city in Fintech Products

How you've been impacted by Miller's Law without realising it, the other psycological principles impacting choice, and mitigating choice friction in fintech products

Hey Fintechers and Fintech newbies 👋🏽

Welcome to another edition of Fintech R&R.

In the news section of the last newsletter, I touched on the trifecta of funding news, which means a trickle-down of much-needed support for SMEs. The £500m+ backing given to SME and gig economy fintechs Uncapped, Iwoca, and Sonovate shows the support of fintech lenders by larger FIs but maybe signals deeper issues ahead for small business and gig economy workers. You can read more about SME's challenges and some fintechs solving those challenges in this previous edition.

While there is an abundance of backing for SMEs, regular readers will know that I like to go a bit against the grain when picking topics to write about. So rather than discussing abundance, I'm diving into scarcity, choice limitation and its application in fintech products. In an age where an abundance of choice, infinite scrolling, and 'frictionless everything' is the norm, it's important to highlight where limiting choice and creating some scarcity can benefit customers and businesses alike.

There is of course, a halloween connection, hence the title, as I missed an edition around the spooky annual gathering of ghosts and ghouls on October 31st, so keep your eyes peeled for some topical movie-related puns but probably no jump scares 👀

Here’s what's in this week's edition:

A Primer on the Paradox of Choice

Psychology of Scarcity

Real-world examples of Choice Psychology

Current and Future Applications of scarcity and psychology in Fintech products

Paradoxical Activity 🤔

“...learning to choose well in a world of unlimited possibilities is harder still, perhaps too hard.”

In my lifetime, up until very recently, I’ve witnessed an upward trend in terms of choice and availability of goods and services. Fruit and vegetable varieties, different types and flavours of coffee, fully ripe/nearly ripe/ripe at home avocados, beer, wine and much more.

Obviously, this isn’t the case everywhere, and there is a bit of Western bias, but I’m looking at it purely through a Western lens for this edition.

And I say, up until very recently, as the pandemic and Brexit both caused supply issues which saw the availability of things like hand sanitiser and toilet roll decrease and the price skyrocket.

Technology has largely seen the same upward choice and availability trend. Make and models of phones, computer and laptop ranges, vacuum cleaners, cameras, microphones and much more. For example, I am writing this article on a Keychron 6, a mechanical keyboard with hot-swappable keys (ability to change the keys), wireless with a wired option and a backlight. This is just one of 100+ combinations of keyboard by the brand that suit different requirements and tastes.

NOTE: This is not a sponsored ad. I’m just a big fan of this keyboard.

FS has been part of this choice explosion. Back in the day, Monzo and Starling were the neobanks on everyone’s lips, Paypal was the default digital wallet, big banks still dominated lending, and Point of Sale lending (BNPL or otherwise) was just a concept in its infancy.

Now tokenization (covered in a previous edition) and digital wallets are everywhere, with large markets in South Asia, East Asia and South America, fintech lenders are popping up daily receiving backing from traditional lenders, and there’s a plethora of big-named PoS finance providers in addition to the one everybody has heard of.

And gone are the days when you land on an e-commerce pricing page and only see a card entry screen. Now it’s card payment, Pay by Bank, PayPal Klarna, AfterPay, ClearPay, ApplePay, GooglePay, SamsungPay etc.

On a macro level there are benefits to a breadth of choice. Choice and optionality can lead to greater competition and a net positive outcome for the consumer, more customer-centric products that solve unique problems, and branding & experience suited to personal preferences.

This is realised in several ways. From niche neobanks creating bespoke branded and niche feature-set banking products to new mortgage providers helping drive down interest rates in line with national changes. A cross-border currency proposition like Wise providing a platform with competitive and transparent FX transfer rates. Credit card propositions like Yonder creating a new lifestyle product aligned with and rewarding a large group of Londoners who regularly eat, drink and enjoy city life.

These are just some examples of the wide benefits of an abundance of choice and healthy competition. Too much choice, however, can be detrimental.

People may be aware of the sunk cost fallacy. The theory is that people who have invested time, effort and money into something are more inclined to stick with a failing initiative because they put weight into the sunk cost they’ve already invested.

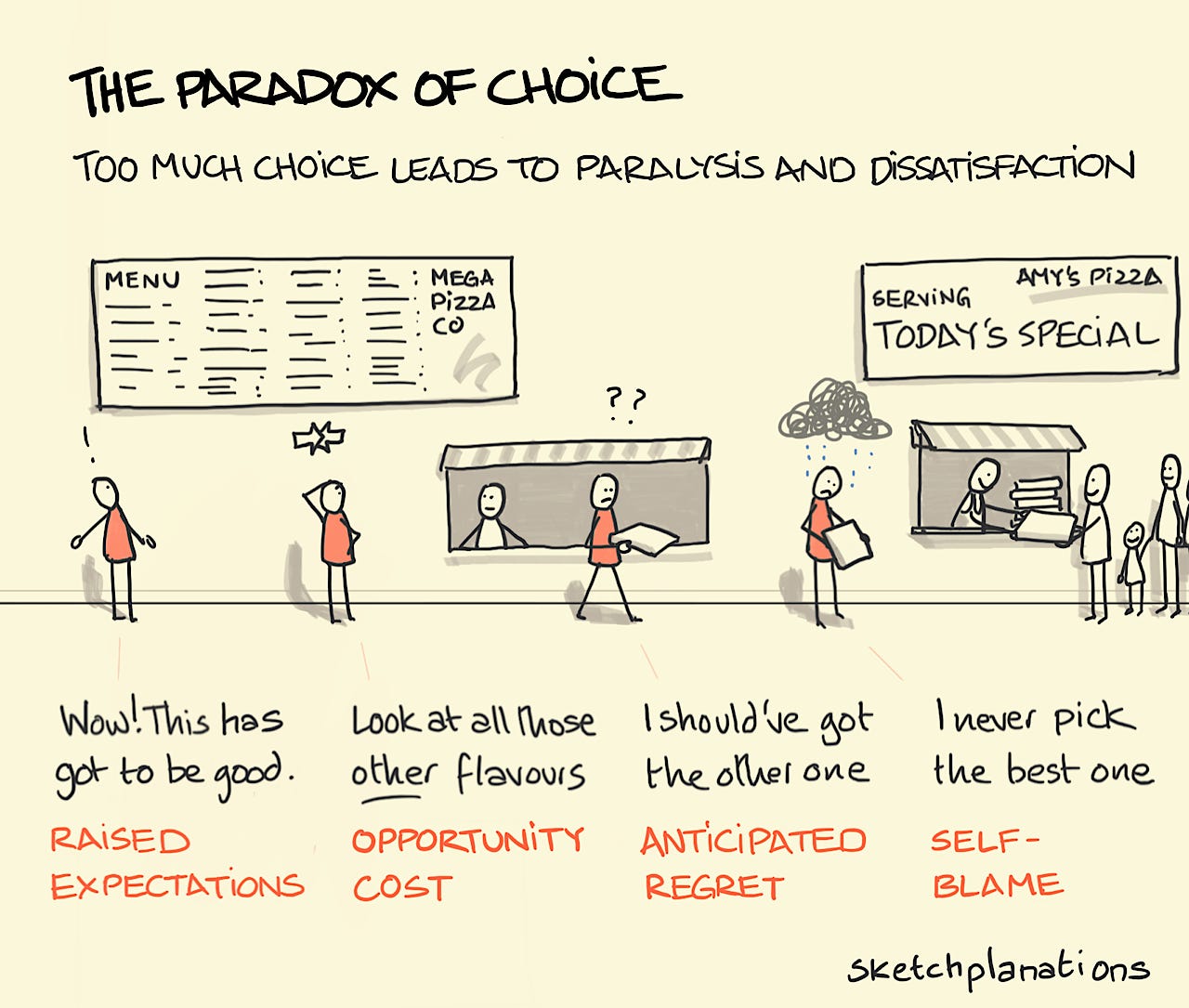

There’s also an equivalent fallacy when it comes to choice called the Paradox of Choice. This phenomenon, written about in great length by psychologist Barry Schwartz in his 2004 book ‘The Paradox of Choice: Why more is less’, outlines the sometimes inverse relationship between the number of choices available and happy, positive outcomes.

One of the overriding outcomes from the book is that there is a tricky balancing act between having enough choices to be satisfied and not having so many options that the process of making a decision becomes debilitating, time-consuming and leads to choice paralysis, which affects the positivity of the end decision.

It’s epitomised by this quote:

“Learning to choose is hard. Learning to choose well is harder. And learning to choose well in a world of unlimited possibilities is harder still, perhaps too hard.”

― Barry Schwartz, ‘The Paradox of Choice: Why More Is Less’

In short, it says that an abundance of choice isn’t all it’s cracked up to be and can often be detrimental to the consumer.

A great real-life example felt by many and outlined perfectly in this article in the Stanford Daily is the inverse relationship between the abundance of choices of romantic partners through modern dating apps and happiness and the phenomenon known as Partner Choice Overload

“What’s fintech got to do with it!”, I hear you ask in your best Tina Turner voice.

Like I said earlier, at a macro level, having more choice when it comes to fintechs and financial products, including selecting a neobank or trying to get a better FX or mortgage rate, is a net positive, but there is a balance to be struck. Having too many choices can lead to choice paralysis, confusion, and negative outcomes.

This is magnified at a micro level when looking at in-app functionality, pricing pages, and things like e-commerce payment options where the abundance of choice can directly impact customer acquisition, conversion, value and ultimately, a fintech’s bottom line.

But before diving into some of the specific benefits of choice restriction and the applications of scarcity in fintech, I want to talk about broader concepts around choice that can be applied regardless of the product type.

Psycho-logy of Choice 🧠

Understanding the overarching behavioural and psychological theory behind choice-making and scarcity is valuable and fundamental to product development, website landing pages, sales funnels and more.

I’ve touched on some of these in previous editions, but this section will bring those concepts and previously untouched ones into a single place.

Hicks Law ⏳

“The time it takes for someone to make a decision increases with the number and complexity of choices.”

I touched on this in a previous pricing deep dive, but here’s a little refresher.

The origin and name of law stems from the psychologist duo of William Edmund Hick and Ray Hyman and their examination of the relationship between the number of stimuli present and an individual’s reaction time to any given stimulus in 1952. They concluded, as expected that the more stimuli to choose from, the longer it takes the user to make a decision on which one to interact with. Users swamped with choices take longer to interpret and decide, giving them work they don’t want.

Generally, the longer it takes and the more complex a decision, the less likely the customer is to complete the desired action, whether taking out a loan, opening an account or completing an e-commerce purchase.

Real-life Example

Modern Sign up pages and OAuth (GoogleAuth)

This is a great example of how the initial bombardment of input boxes asking for First Name, Surname, age, Email Address, has been simplified on many sites into a Single Sign On/Single Sign Up link using existing onboarding and authentication services like Google and Facebook. This means sign-up is two clicks rather than laborious text entry, and sign-in is one click, reducing decision complexity and number of choices and increasing conversion.

Miller's Law 🔢

“The average person can only keep 7 (plus or minus 2) units in their working memory at a time.”

Miller’s Law was proposed by George Miller in 1956 in his paper “The Magical Number Seven, Plus or Minus Two: Some Limits on Our Capacity for Processing Information.” and was developed during a time when researchers in the cognitive psychology field were beginning to understand the processes of human memory and information processing.

His research indicated that when we are presented with more than 7 items of information at a time, we may have difficulty processing and remembering all of it. This is a heavily cited principle in the world of cognitive psychology due to design implications across a range of areas, including business and education.

The implications of the ‘magic number 7’ can be seen across marketing campaigns, app UX, websites, surveys and more, with many using this principle to inform the breadth of options, statistics and key features to present to customers to make it easily absorbable and impactful.

Real-life Example

Chunking a phone number or first-time tutorial to increase Time To Value (TTV)

When it comes to Miller’s Law, limiting the number of choices is ideal, keeping them in the 3-5 range, but when this isn’t possible, ‘Chunking’ is the go-to antidote. Chunking is the process of separating a plethora of images, text, data or other info into chunks rather than those individual units so they are easier to process.

A classic example is a mobile number. A typical UK mobile number starts with 07, followed by 1-5 or 7-9 and 8 random digits. So, 11 digits in total.

Most people will chunk their numbers differently rather than remembering all 11 digits in sequence.

Demonstrate telling me your phone number right now.

Odds are you didn’t stream the 11 digits monotone, and it was probably something like this:

077 - 388 - 28541 (3, 3 and 5).

This is just a made-up number, btw, but I’ve applied the chunking technique that I use on my actual number.

Some use 07738 - 828 - 541 (5, 3 and 3).

I’d be interested to know other chunks folks use.

The point of chunking is to break these 11 units into 3 chunks, making it easier to remember so you’ve chunked and experienced Miller’s Law without even realising it.

A product example of chunking is splitting a lengthy initial product tutorial into separate component chunks. The go-to example used by many is Slack and its in-app tutorial that guides the customer through the different areas of the product, navigating through 5 different chunks of the product, making it simple for the customer to get started and postponing all ‘non-critical’ tasks until later down the customer’s journey.

Gestalt Law of Common Region 🔲

“objects located within the same boundary are perceived as being grouped together.”

The Gestalt Principles are a set of laws of perceptual organisation which describe different facets of human perception and how our brains make sense of visual information.

The Gestalt principles – Gestalt being the German word for “unified whole”–were developed by German psychologists Max Wertheimer, Kurt Koffka, and Wolfgang Kohler in the 1920s.

The trio identified a set of laws that address the patterns and perceptions found in elements and the way humans perceive and process visual information.

Some of the key ones are visualised brilliantly here:

All the laws are relevant in some way to choice, but one that’s particularly relevant is the Law of Common Region, which states that when objects are located within the same boundary, we perceive them as being grouped together.

The Law of Common Region is a great way to help customers distinguish between a range of options and group them into logical choices and can be used in conjunction with some of the other Gestalt principles to make choices leaner and simpler for customers.

Real-life Example

Pricing grid page and Apple’s Home screen

There is, of course, some Hick’s Law involved when it comes to pricing pages and some Decoy Pricing tactics with limiting and pronouncing differing options, but there are also some Laws of Common Region. For example, many pricing pages will use a grid and differentiate between the different column options so it’s clear which features relate to which option.

As the app store and iPhone became more popular, more developers created and published apps, making home screens a bit noisy. In anticipation of further growth, Apple developed the ability to create squares around groups of similar apps, making it easy for customers to navigate their home screens, download apps and have some level of organisation whilst still exploring new ones.

The Scarcity Principle 👻

“Opportunities seem more valuable when their availability is limited”

This is a commonly understood concept and confirmed by many behavioural scientists, including Robert Cialdini in his book “Influence: The Psychology of Persuasion”, that scarcity increases desirability.

It means scarcity, and by definition, exclusivity can be used to help steer customers to a particular choice and plays on most people’s desire to have items and experiences that are exclusive and limited.

Now that I’ve said ‘limited’ it’s clear that every limited edition item is an attempt to convert you by using the scarcity principle, but don’t worry, we’ve all been caught up in it at one stage or another.

I myself have a costly, limited edition Dark Knight picture sitting at the back of my cupboard.

Cialdini also cites competition as a factor in scarcity, stating, “Not only do we want the same item when it becomes scarce, we want it most when we are in competition for it”. This means exclusivity and urgency is a winning combo and can help steer customers towards a particularly favourable choice OR encourage product builders to create more bespoke limited tiers of memberships or exclusive limited products.

Real-life Example

Founding memberships and crowdfunding

Early-stage products use founding memberships to encourage customers to sign up for slightly pricier memberships, with perks using scarcity (limiting the number of memberships) and exclusivity to lure customers into becoming lifetime members.

Similarly, crowdfunding campaigns use ‘early access’ badges to denote exclusive early investing and crowdfunding targets to create urgency and encourage people to invest before the allocation fills and the funding round completes.

Applications in Fintech 📱

The real-life examples make clear some of the ways fintechs use, consciously or unconsciously, some scarcity and choice psychology to acquire and keep customers. I’ll outline the ones that I personally and professionally admire here but also add a couple of areas where fintech products could use these principles in the future to make choices easier for customers.

1️⃣ Waiting Lists and ‘Golden Tickets’

A great way to generate buzz for an early-stage product before it is even built is to set up a landing page that summarises what the product will be and who it’s for and allows potential customers to sign up to be first in line to use the app.

Letting potential customers be the first ones to use the app when it comes out creates the sense of exclusivity and scarcity people look for.

An even better way to create buzz is to give these early adopters the power to get their friends and family involved to allow them to sign up and jump the queue so they all get access simultaneously.

After all, getting early access to a bar is no fun if all your friends get left behind.

This (the waiting list and the golden ticket idea, not the early bar access), is exactly what early Mondo Monzo did on their customer growth journey, going through different versions of the waiting list gamification process and eventually discontinuing the Golden Ticket scheme once their brand became more widely recognisable which was in no small part down to leveraging exclusivity and interest.

I’d love to see more interesting ways to showcase the early versions of the product, get sign-ups and eventually pull some viral growth levers using the Scarcity Principle. If you’ve seen some good examples recently, please send them across.

2️⃣ Pricing Pages

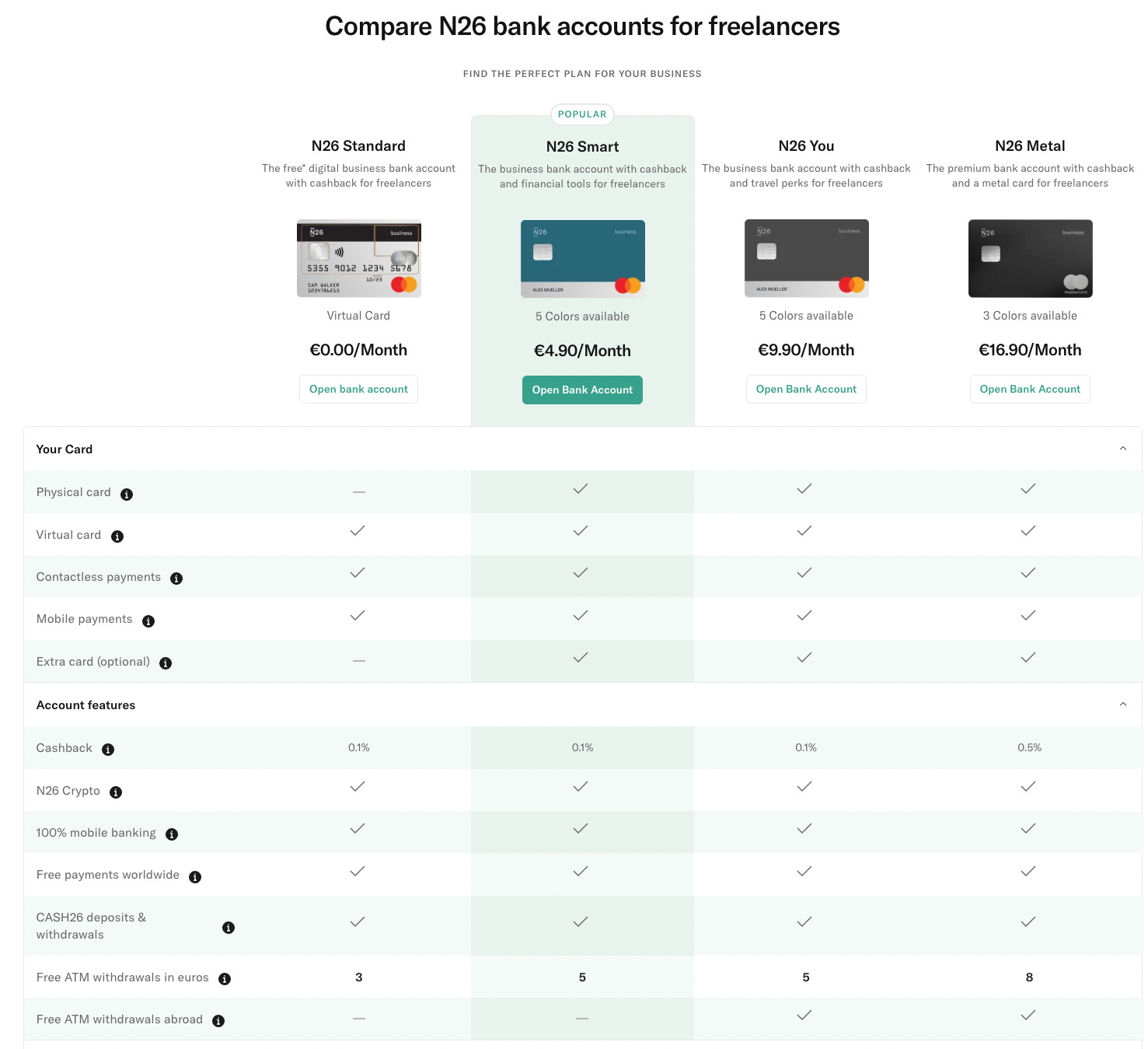

An area that, for me, drastically varies in quality and impact is many fintech pricing pages and the use of Hick’s Law and the Law of Common Region to make it easy for the customer to pick the right option. A positive example is N26, which uses chunking to group the extensive list of features into logical sets less than the magic number 7 and uses the Law of Common Region to make their cheapest paid option stand out.

There are some bad examples out there as well. I’m not going to name and shame, but those pages with 10-20 ungrouped features on the y-axis of the grid that don’t make clear the popular or ‘best’ option are making it easy for customers to browse and then leave the page never to return.

3️⃣ Mitigating Miller’s Law: Transaction Feed and Spending Categories

There are two areas of fintech that I predict we’ll see some changes around the mitigation of Miller’s Law and processing information.

Spending Analysis and associate categories

The Transaction Feed

Neobanks have been waking up to the fact that providing what is often a loss-leading personal finance management feature can be beneficial in understanding where else customers bank, how they separate different accounts for different uses, and to get a better, FULLER picture of individuals’ finances. But one area that has been difficult to crack is nailing the spending categories. They often go way over the magic number of 7 and beyond that point, becoming a bit useless, and the importance of those categories is diluted.

Making either a bespoke set of 5-7 categories based on customers’ spending or ensuring an all-encompassing group of categories that cover most customers will be a progressive step for neobanks who will inevitably eat up a lot of the PFM space.

Ahhh, the transaction feed.

Frankly, it is a mostly ineffective use of real estate in a banking product. In years gone by, this + the account balance was the default homepage for most digital accounts. It’s now being pushed lower down the prominence stack. One way to bring some value back to the vanilla transaction feed is to split up the reams of transactions with relevant offers, discounts, spending analytics, and relevant calls to action.

An example of a fintech app that does this reasonably well is the American Express app. It splits up groups of transactions with different lifestyle offers, reward points opportunities and other relevant actions.

I anticipate more enriched transaction feeds on the horizon, breaking up the long stream of transactions and using relevant decision-making to split up the large batches of data that customers have to trawl through.

4️⃣ Digital Bank ID to speed up lending

The first point in the psychology of choice section was about Hick’s Law, the complexity and number of choices frustrating customers and how SSO, along with simplified sign-up pages, removed unnecessary decision-making, leading to higher converting landing pages.

This is still an issue when it comes to consumer and SME lending.

The benefit of Google’s SSO is that in a couple of clicks, the customer can create an account and share some key bits of info without going through five screens of forms.

With consumer and SME lending, Google SSO saves a minimal amount of time in the grand scheme of things, as for each lending application, the customer has to provide for every individual application through a new institute.

Natwest and Lloyds both have digital ID initiatives at different stages, and I think the first large-scale beneficiaries of this will be SMEs who can use it to streamline the digital onboarding and application process to obtain timely products and services, including finance, to help their businesses thrive. This will not only help the onboarding process but also make the product choices a lot more tailored, making the consumer decision easier.

Outro

To some, these concepts will seem completely new. To others, it will be treading familiar ground.

I’ve gone fairly deep on the subject of choice and scarcity, but I’ve barely scratched the surface when it comes to overall UX. But to be fair, it wouldn’t be my mastermind specialist subject. That’s why embedding dedicated UX researchers and designers into fintech teams is vital.

It’s also the responsibility of the product team and product leaders in fintech to understand these concepts, how they relate to the problems being solved for customers and the best way to approach things like choice limitation, information processing, perceptual organisation, and scarcity to drive adoption & growth.

These are all things that need to be considered when building a roadmap and developing a viable product that tie back to the overall strategy.

But closing out with the original header around abundance and seemingly unlimited options, especially when it comes to financial products.

Sometimes more is…well…more. More financial products mean more competition and a more competitive rate for customers.

But when it comes to aiding decision-making, increasing conversion and generally leaving customers satisfied with their choices, less is definitely more, and what I’ve outlined serves as the evidence to prove it.

Favourite bits of news

Oxbury Bank secures £100m - As I was writing this, another sign of backing For SME finance landed on my lap with Oxbury Bank, the agricultural bank providing asset finance and secured lending to farmers, and landed £100m of backing from the British Business Bank.

YouLend and Amazon strike Embedded Finance deal - I predicted big tech firms like Shopify and Amazon partnering to provide more funding options to its merchants back in the embedded finance edition. While I assumed they’d use someone like Pipe to deliver Revenue-based finance options for their customers, the trusted provider YouLend has secured a deal to provide a merchant cash advance facility that will benefit all three parties. Amazon, YouLend, and more importantly, Amazon UK merchants.

fashion rules apply in fintech as well lol